Foreword

This is a quick note, which tends to be just off the cuff thoughts/ideas that look at current market situations, and to try to encourage some discussions.

The Iran war has been going on for about two and a half months now, and despite the ceasefire, I am getting concerned. Again.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Not that quick

Technically, this was branded as a quick note, but the Iran war is a lengthy topic, so this is going to be a long post. Start your white noise machine and get comfortable — I expect half of you to be asleep before reaching the end of this post.

Quick background

For those who haven’t been following – The USA and Israel attacked Iran in a surprise attack on February 28th, 2026. This is despite ongoing diplomatic meetings in Geneva where some progress was made.

The attacks resulted in retaliation from Iran on multiple Gulf Cooperation Council (GCC) member countries, with severe damage dealt to US military bases as well as various energy (crude oil, refined products and natural gas) infrastructure in the region.

In addition, Iran also announced the closure of the Strait of Hormuz, a critical maritime chokepoint for shipping energy products out of the GCC countries, and shipping their imports in. Currently, traffic through the Strait of Hormuz has dropped from around 100-150 per day, to 0-20 a day — only ships that pay a toll to the Iranian regime and receives approval from them are allowed to transit.

Naturally, this has led to a severe shortage of various energy products in the world. As a response, the USA has also imposed a retaliatory blockade of Iranian shipping vessels.

Economic impact

Prior to the war, the Strait of Hormuz was used to ship around 20million barrels of crude oil per day out of the Gulf countries. Global crude oil consumption on a daily basis is around 100million barrels, so the closure of the Strait of Hormuz immediately curtailed around 20% of global crude oil intake.

At the same time, the Gulf countries have over the years started developing more value added energy related services, such as exporting refined products, as well as various oil refining byproducts such as helium, sulphur and various fertilizers or fertilizer inputs.

While some of these products are still being exported today via bypasses, such as the East-West pipeline in the Kingdom of Saudi Arabia, taking into account all bypasses still leave results in a shortage of around 10-13 million barrels of oil from the region. To be clear — some analysts have falsely claimed a much higher rate of bypass, this is easily disproved by just looking at the shut-in of production in the Gulf countries (i.e. how much less crude they are producing a day). You simply cannot export something that you have not extracted yet.

At the same time, there are some who claim that because Very Large Crude Containers (VLCCs) can ship around 2million barrels of oil each, we only need ~10 ships to transit a day, a number seems to be already happening. This is, in my opinion, simply wrong.

The easiest counter argument is simply this — prior to the war, 100-150 ships transit per day. If we only needed 10, what were the other 90-140 doing? They certainly were not all cruise ships!

The fact of the matter is that there are 3 main types of ships involved – crude tankers, gas carriers and bulk carriers. You cannot load crude oil on gas carriers or bulk carriers, you cannot load natural gas on crude tankers or bulk carriers, and you cannot carry bulk goods in crude tankers or gas carriers. As a result, many ships tend to enter or exit the region empty (i.e. crude and gas carriers enter empty and leave loaded).

At the same time, the region exports a lot more than just crude oil. The world is also in need of the region’s fertilizer and fertilizer inputs, helium and various other refined oil products.

Finally, the main reason why the region even bothers to export all these goods, is so that they can earn foreign exchange to pay for imports that they actually want. If the flow of imports is completely curtailed, it seems their need and will to export will also be reduced.

A simple empirical proof that the current limited number of transits is nowhere near enough is the number of ships entering the region (as opposed to exiting). Unfortunately, I can’t find a clean graph that shows the data, but if you are willing to dig through news articles over the past few weeks, you’ll notice that almost all the ships transiting are exiting the region, not entering. Without new ships entering the region, existing ships within the region will eventually dwindle down to nothing and the export flow will pause/diminish.

Ships stuck in the region

As mentioned above, most of the ships transiting the strait currently are east-bound (i.e. exiting the region). The number of ships estimated to be stuck within the region unable to get out is around 1500-2000 ships, so at the rate of ~20 a day, we’ll need a few months before all of them are out.

Some of these ships have been in the region for months, and are running low on food, fresh water and other necessities of life, leading to potential humanitarian disasters. Countries in the region are reluctant to provide too much aid to these ships for fear of angering Iran, and likely also because they themselves have been starved of imports for a while now.

Shut in

More importantly, given that the ships in the region have been there for almost 3 months suggest that those that were planning to ship exports out of the region are already loaded.

From my understanding, crude oil and natural gas extraction while very different in nature, share some characteristics. In both cases the output needs to be stored in specialized containers. Given that existing ships in the region are likely fully loaded, newly extracted oil and gas will need to be stored in storage containers on land. These tend to be relatively limited in capacity and many estimates I’ve seen suggest that most of the region’s land capacity are filled up.

As a result, oil and gas wells need to be shut in, i.e. temporarily closed. When an oil or gas well is shut in, there is a chance that damage to the well or equipment is sustained, resulting in reduced pressure and thus reducing the amount of extractable oil/gas. In extreme cases, the well may become completely inoperable.

The longer these wells are shut in, the higher the chances of problems in the future. While likely most of the problems can be overcome with enough effort, this does incur significant investments as well as time — some estimates I’ve seen suggest that from the date of wells reopening, it may take a year or more before the region’s energy exports get back to pre-war capacity.

Now, add in the fact that many ships outside the gulf region have moved to other parts of the world to do business, and land storage are full, even if the war magically ends today, it’ll likely take a significant amount of time for ships to return to the region, relieve the land storage of their contents, before we can even think of reopening the wells (which is when the one year or more timer starts).

Bypass

A quick word about the bypasses. There are 3 main bypasses that are operating:

- The East-West pipeline in Saudi Arabia.

- The Habshan-Fujairah pipeline in the United Arabs Emirates (UAE).

- The Iraq-Turkey pipeline.

All three pipelines are operating but at various levels of utilization.

The East-West pipeline takes oil out of the Persian Gulf (which opens into the Strait of Hormuz) and into the west coast of Saudi Arabia, the Red Sea. The Red Sea has two egresses — to the north, there is the Suez Canal and the Mediterranean and Europe, and to the south there is the Bab el-Mandeb which then leads to Asia.

Unfortunately, the Bab el-Mandeb is bordered by Yemen, where the Houthis are situated. The Houthis are allies of the Iranian regime, and have previously managed to successfully disrupt shipping out of the Red Sea via the Bab el-Mandeb. While the Houthis have not done much so far in this war, they have made verbal promises of coming to Iran’s aid if/when requested. There is speculation that the Houthis are not keen to enter the fight — they last closed the Bab el-Mandeb in 2023 in a conflict that is technically still ongoing, but paused due to a ceasefire that began in 2025. Whether that is true, or whether the Iranians have simply been holding the Houthis back in reserve is unclear.

Thankfully, the Red Sea has another egress via the Suez Canal. However, the canal is man made and has much smaller limits on how many ships can transit in a day. At the same time, the canal is narrower than the Bab el-Mandeb, and the largest ships than can transit are SuezMax ships, which hold roughly 1million barrels of crude at most, half of what a VLCC can hold.

The Habshan-Fujairah pipeline is relatively new and still being ramped up. However, Iran has recently redesignated the boundaries of the Strait of Hormuz so that it includes Fujairah, the two eastern (out of the Persian Gulf) endpoint of the pipeline. At the same time, there are reports that at least one ship near Fujairah was seized by “unauthorized personnel” and is being taken towards Iran.

The Iraq-Turkey pipeline has been in and out of development for a while now, and from my understanding, while it is operational, it has very low capacity and there are technical/legal issues to ramping that up quickly.

All 3 pipelines also share a similar downside — they are all within range of Iran’s missiles. While Iran has not made any moves in this area, they have promised that if more attacks were to initiated on Iran, they’ll hit all energy infrastructures in the region, which likely includes these 3 pipelines.

Agriculture

The Persian Gulf region exports a large amount of fertilizers and fertilizer inputs which is used all around the world, including here in the USA. As a result of the closure, prices of fertilizers has increased dramatically.

Each agricultural growing region in the world are typically split into multiple plantings. These planting periods are different depending on the crop and the region of the world, but as a sort of crude estimate, there are 2 plantings during the summer in the USA. The first is around April to May, and the second is around July to August.

My understanding is that for the April/May planting, most farmers have already ordered their fertilizers before the war started and so are relatively unaffected. However, some crops require additional fertilizers after they are planted, and that may be affected. Also, if the war drags on long enough, the July/August planting may also be affected, since farmers don’t typically store fertilizers for more than a few weeks, though they may have been able to lock in pricing from before the war.

Other than fertilizers, the business of agriculture is also heavily dependent on fuel, as modern farming relies heavily in machinery to do most of the heavy work. The increase in fuel prices due to the closure adds significant costs to farmers’ operating expenses.

At the same time and unrelated to the war, this year is forecasted to be a strong El Nino year. While El Nino affects different parts of the world differently, my understanding is that El Nino will be a net negative for global agricultural production.

Finally, there is a pretty serious drought affecting large parts of the USA currently, which is affecting crops.

Put all these together, and we get pretty substantial impacts on food supplies. For example, wheat prices went limit up (went up by the maximum of ~7% in a single day) on May 12th, as farmers reduce the amount of wheat they plan to grow this season. At the same time, prices of various other agricultural products such as sugar and corn are also pushing towards recent highs, for similar reasons.

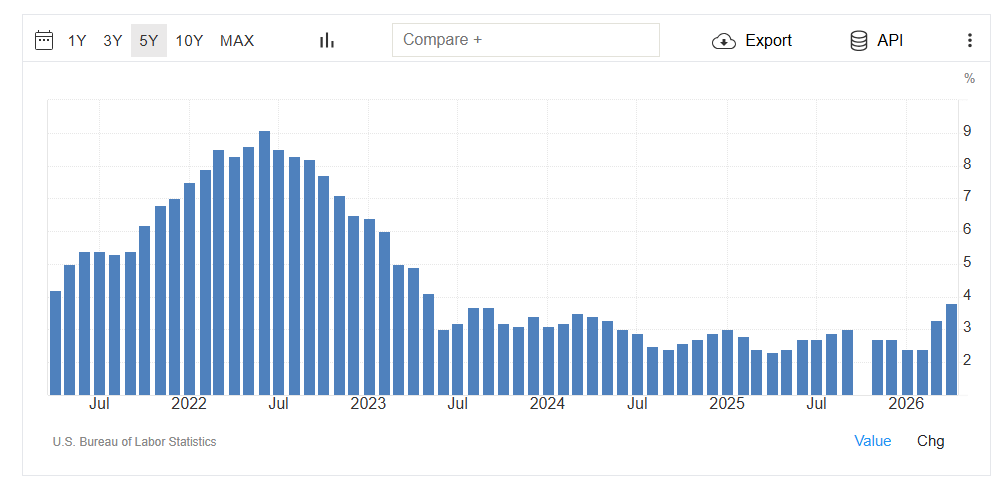

Inflation

Covid in 2020, the Russia/Ukraine war in 2022 and the government’s response to both events led to high inflation in the USA starting in 2021. That reached a peak of around 9% in 2022 before slowly coming down.

However, the disinflationary trend of lower inflation was interrupted in early 2025 after the announcement of severe tariffs imposed by the US on the rest of the world, and resulted in steadily increasing inflation until around August when most of them were rolled back or scaled down.

With the Iran war and the closure of the Strait of Hormuz, fuel prices has gone up significantly throughout the country, and as discussed above, food prices are starting to go up as well.

It is important to note that while fuel prices are the most directly linked to increased crude oil prices, crude oil is involved in pretty much everything we interact with daily, from the diesel used to transport goods, to jet fuel used for planes, to fertilizers for our crops, to asphalt lining our roads, to material used for clothing, furniture, etc.

Because some of these products are very far downstream from crude, involving multiple steps of refining and manufacture, increased crude prices may take weeks or even months/years before the prices of the final products are affected.

The latest consumer price index (CPI) inflation report jumped to 3.8%, the highest since mid 2023. At the same time, producer price index (PPI) inflation hit a scorching 6%. Given that producers, like all businesses, need to make a profit to survive, there is a good chance that the increased in prices faced by producers will eventually be passed on to consumers.

Peace demands

Currently, Iran appears to believe they are winning the war, as the demands they’ve made just to begin peace negotiations include what the US would likely consider red lines:

- Lifting of the US blockade.

- Iran retains control of the Strait of Hormuz.

- Lifting of all US sanctions on Iran.

- War reparations for damages dealt by the US and Israel.

- Release of frozen Iranian assets.

- No discussion of Iranian nuclear issues until after the conflict has ended.

Given that these demands essentially removes all US/Israel leverage in any future negotiations, and effectively amounts to a US/Israel unconditional surrender, it’s hard to imagine that the US/Israel will look kindly on the demands.

On the other hand the US demands for the same peace negotiations to begin:

- Long term nuclear moratorium on all Iranian uranium enrichment, with the dilution or removal of existing nuclear material within Iran.

- Iran end all support for regional proxy groups like Hezbollah, Houthis and Hamas.

- Reopen the Strait of Hormuz by the Iranians, though the US may maintain its blockade.

While the US offers the possibility of sanction relief and return of some/all frozen Iranian assets, it is pretty clear that their list of demands will be entirely unacceptable by the Iranians as well.

At the core, the facts are:

- Within a year, the US/Israel launched two surprise attacks on Iran during diplomatic negotiations, once in June 2025 (the Twelve-Day war) and another time in Feb 2026 (the current Iran war).

- Both times, the US and Iran were in the middle of negotiations centered around US sanctions on Iran as well as Iran’s nuclear enrichment programs.

As such, it seems natural for Iran to be suspicious of another peace overture from the US/Israel, and likely they’ll want some guarantees that it’s not another trick/trap.

Since there are no practical ways for any entity on Earth to ensure/guarantee that the US/Israel will not launch a third surprise attack, Iran likely wants to retain some amount of coercive force to defend itself. The two main prongs of that defense posture would be control of the Strait of Hormuz, and thus control over roughly 20% of crude oil used globally, as well as a credible nuclear deterrent. Both of which the US demands to be removed from the table.

Time’s running out

While only about 10% of daily crude oil consumption worldwide is affected, the fact of the matter is that the world simply cannot operate without crude oil and even relatively small changes can have significant impact. It is important to note that historically, OPEC has generally adjusted crude oil production up or down by a few hundred thousand barrels a day at a time, and even those adjustments tend to have significant impact on prices. We are currently seeing a reduction of supply 10 times higher.

JP Morgan recently published an update estimating that at the current rate, the world will face significant operational stress by June, and by September we’ll hit operational minimums. It is important to remember that while the world has large buffers of crude oil stored away for an emergency such as this, the reality is that much of those oil is simply not accessible — tanks need a minimum amount of oil to operate and pipelines cannot operate if they are empty. While we can technically drain tanks and pipelines completely, the process is slow and tends to result in irreversible damage. Hence the notion of operational minimums — if storage levels fall below that, we simply cannot efficiently (or at all in some cases) retrieve the stored oil.

As of today, June is just 2 weeks away, and September is only 3 more months after that. We simply do not have a lot of time left.

Hopefully the USA, Israel and Iran can reach a peace agreement soon, but given that the current ceasefire started in early April and both sides are still so far apart, I am genuinely worried.

Export ban

Before we end, a quick word on a potential export ban. Some have suggested that because the USA is “energy independent”, if push comes to shove, we can simply impose an export ban on crude and/or its refined products, so the impact on Americans will be significantly reduced.

While that idea isn’t completely wrong, recall from above that crude is used as input for a wide variety of things, many of which are not produced in the USA. An export ban will necessarily increase the price of crude and its products outside of the USA, which then will increase the cost of our imports. Remember also that those imports necessarily must be shipped in or flown in, and ships and planes run on fuel. Fuel that is typically topped up at the point of origin, i.e. outside of the USA, and thus more expensive.

At the same time, an export ban will shift a lot of the pain from Americans to the rest of the world. This will likely lead to significant financial/economic stress outside of the USA. Given that the USA is tied closely to the rest of the world via trade links and services, if the rest of the world is in severe distress, we’ll likely be impacted too, via increases in the price of imports, via decrease in the demand of our exports and our digital services, etc.

So, strictly from an energy perspective, the take isn’t completely wrong, but it is not a panacea, and Americans will be impacted, even if the ban is instituted.