This is a quick note, which tends to be just off the cuff thoughts/ideas that look at current market situations, and to try to encourage some discussions.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Covid-19 strikes back

Since around early July, stocks have been trading mostly sideways with a slight downward bias in the previous week. Yesterday (7/19), stocks took a ~1.5% dive, while volatility, as measured by the VIX, peaked at over 24 from a sleepy sub-18 print last Friday. This decidedly reddish hue of green caused a bit of a stir, especially since it is hitting in the middle of summer, a period traditionally marked by quiet markets as traders are busy with their vacations.

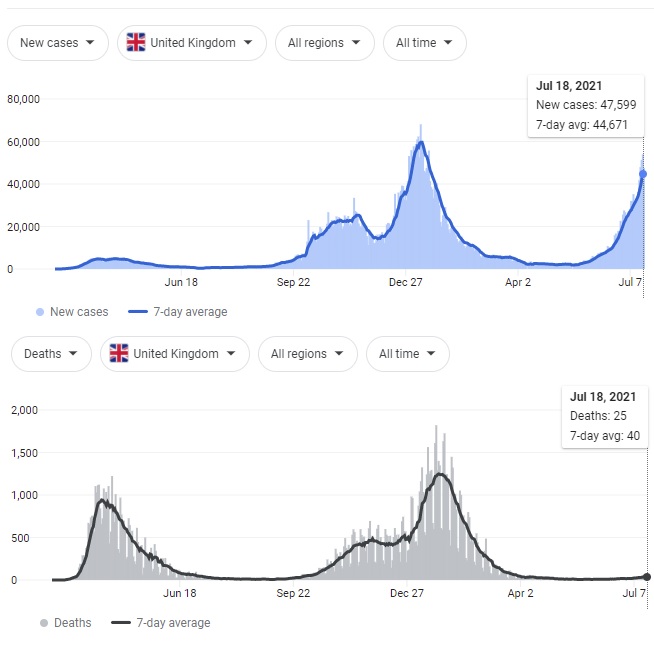

The financial news media is abuzz with suggestions that a rise in Covid-19 cases, this time by the delta variant, is to blame. Multiple countries are seeing an uptick in Covid-19 cases, with the UK especially apparent — cases in the UK are at 70% of all time highs (around 48k cases/day, compared to around 68k/day at the highs), and appears on track to take out the highs in a week or two. UK health officials and media are flirting with the idea of lockdown again, though Boris Johnson did not relent, with Freedom Day finally arriving yesterday.

The rise of the vaccinated

Despite the seemingly grim news, there is a ray of hope. While cases have been rising, death toll from Covid-19 has been surprisingly muted:

UK daily Covid-19 cases and deaths, courtesy of Google.

Some have speculated that this is due to the high rate of vaccination in the UK (at 70% of the population having at least one dose, it’s one of the highest in the world), while others have suggested that better treatments available, now that doctors and researchers have had more time and experience. Regardless, based only on the UK’s numbers in the past 7 days, the current death rate (1) for Covid-19 is lower than that for the flu (2).

A few random countries I picked show similar trends (cases up but deaths down) or better (cases and deaths both down). None of the 10 or so countries I randomly tried saw increasing death rate (as a ratio of case count).

So, unless that death rate suddenly spikes dramatically (3), it seems like the market may be overreacting slightly, assuming their only concern is the rise of Covid-19.

The cyber menace

If only that was the only thing we need to worry about. Over the weekend, a report came out suggesting that some of the major cyber attacks on US soil (4) in recent memory had links to China. President Biden made it official yesterday in an official White House press release, and the statement was backed by a few American allies.

Perhaps I’m still suffering from PTSD (5) due to the trade war of 2018, but this has undertones of a time when I’d rather not revisit, especially in light of the recent tensions due to big tech regulations, human rights, etc.

Hopefully a peaceful diplomatic solution can be found, but at least in the short term, it’s another thing to think about.

The last meme

Something that I’ve prognosticated on since last July (6), was the return of normalcy. The thesis being that with everyone cooped up at home, there is a natural draw towards more retail trading, but with reopening (7), “other stuff” will naturally take up our time, which should reduce retail trading volumes. And if retail traders were mainly the culprits bidding up markets (specifically meme stocks), then a lack thereof of such may portend dark tidings.

So far, this is sort of happening — meme stocks hit a crescendo in February/March and have been mostly leaking lower ever since.

Finally, with the end of fiscal support, especially the eviction/foreclosure moratorium, around the end of July, the impetus is there for more folks to hunt just a little bit harder for their next job, and recent joblessness numbers are reflecting that.

And well, it’s just harder to day trade meme stock options when you’re working, y’know?

Attack of the karma

Of course, now that I’ve typed this all out (despite the tone and date of the post, I’m actually typing this on the evening of July 19), you can bet that the markets will open (7/20) green and make new all time highs before lunch (8).

Because. Just because.

Footnotes

This is not a perfect measure — deaths are strictly a “lagging” indicator, while a non-trivial number of people are probably misclassified either way (died from Covid-19 labelled as died from other causes and vice versa). At the same time, there’s probably a good number of people who are infected but are not captured by official statistics for various reasons.

It might! Again, deaths necessarily lag infections.

Can you actually say a cyber attack is on “US soil”? Seems kinda weird?

I happen to be trading FX algorithmically in 2018, and well, you always trade FX with leverage. Huge amounts of leverage. Makes for very unpleasant blood pressure graphs whenever ex-President Trump tweets anything about the trade war.

If your predictions don’t come true, try, try again. Eventually they will come true. Or everyone will have died of old age and nobody will remember anyway.

Remember folks predicting that we’d be reopening in July… 2020?

Absolutely not investment advice. Though if you do bet on it and made money, you’re welcome. 🙂

There are some who think that stocks are gambling, that trading stocks is, essentially, a zero sum game. In some sense, they are right, but the truth is more nuanced than that.

How do we reconcile the idea that trading stocks are a zero sum game, with the very real fact that a non-trivial number of financial fiduciaries encourage their clients to invest in stocks?

Can you even “invest” in something that is a zero sum game?

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Flip flopping

Let’s say we have 2 buddies, Alex and Blair. They each have $1,000 as they begin their journey:

Total Cash (dollars)

Total Assets (units)

Asset value (dollars)

Debt (dollars)

Net Worth (dollars)

Alex

$1,000

0

$0

$0

$1,000

Blair

$1,000

0

$0

$0

$1,000

Now, let’s say they have a brilliant idea(1) — they’ll create a brand new asset, let’s call it Kelpie, and they have a brilliant, fool-proof way to get rich, together. First, Alex starts with 100 Kelpies, conjured out of thin air, and they will value it at $1 each.

Total Cash (dollars)

Total Assets (units)

Asset value (dollars)

Debt (dollars)

Net Worth (dollars)

Alex

$1,000

100

$100

$0

$1,100

Blair

$1,000

0

$0

$0

$1,000

Price of 1 Kelpie: $1

Voila, our two friends, combined, are now $100 richer. But they have grander plans than that! Alex next sells 50 Kelpies to Blair at $1.10 each. The “market value” of each Kelpie is now $1.10.

Total Cash (dollars)

Total Assets (units)

Asset value (dollars)

Debt (dollars)

Net Worth (dollars)

Alex

$1,055

50

$55

$0

$1,110

Blair

$945

50

$55

$0

$1,000

Price of 1 Kelpie: $1.10

Now, our two friends are, combined, $10 richer — Blair is still worth $1,000, but Alex made another $10. Well, this is a mutually beneficial relationship, and so far, only Alex is making hay. To make it up to Blair, Blair now sells 10 Kelpies to Alex, at the princely price of $2 each.

Total Cash (dollars)

Total Assets (units)

Asset value (dollars)

Debt (dollars)

Net Worth (dollars)

Alex

$1,035

60

$120

$0

$1,155

Blair

$965

40

$80

$0

$1,045

Price of 1 Kelpie: $2

Notice how both Blair and Alex are now worth more than their initial $1,000. More interestingly, even though Alex bought Kelpies from Blair at a much higher price than when they sold it to Blair, Alex actually “made” $45! I think we have a winner here!

Alex and Blair continue trading between themselves, with Kelpies trading at higher and higher prices. Eventually, we hit this state, where Kelpies are $100 each:

Total Cash (dollars)

Total Assets (units)

Asset value (dollars)

Debt (dollars)

Net Worth (dollars)

Alex

$2,000

20

$2,000

$0

$4,000

Blair

$0

80

$8,000

$0

$8,000

Price of 1 Kelpie: $100

Now, we have a problem. Blair is supposed to buy Kelpies from Alex this round, but they are out of cash! That’s fine, Blair takes out a loan of $1,000 against their “assets” of $8,000 — that’s only a 12.5% loan-to-value (LTV), which is generally considered “safe” by most banks. Blair then use the newly acquired cash to buy more Kelpies from Alex at $200 each.

Total Cash (dollars)

Total Assets (units)

Asset value (dollars)

Debt (dollars)

Net Worth (dollars)

Alex

$3,000

15

$3,000

$0

$6,000

Blair

$0

85

$17,000

$1,000

$16,000

Price of 1 Kelpie: $200

Notice how Blair’s net worth doubled, despite taking out a loan, and spending cash to buy Kelpies.

Our two friends continues trading Kelpies between themselves, taking out loans if needed if one of them runs out of cash when it’s their turn to buy. By trading Kelpies back and forth, both of them managed to greatly improve upon their net worth. Their last trade has Kelpies valued at $1,000 each. Houston, we have liftoff!

Total Cash (dollars)

Total Assets (units)

Asset value

Debt (dollars)

Net Worth (dollars)

Alex

$10,000

40

$40,000

$5,000

$45,000

Blair

$2,000

60

$60,000

$5,000

$57,000

Price of 1 Kelpie: $1,000

Car shopping

At some point, Blair decides they want to buy a new car. And since they are rich now, only a fancy car will do — a fancy car that costs $50,000. It’s going to hit their net worth hard, but what the hell, you only live once! Besides, Blair has found the secret infinite money cheat to life!

Unfortunately, the car dealership won’t take Kelpies (they simply do not see the transformative nature of Kelpies), and they want cash instead. So Blair went to Alex, and asks (nicely) if Alex would buy some Kelpies from Blair at, say, $1,100 each, so that Blair can raise $50,000 for the new car. However, Alex does not have the cash, and is unwilling to take out such a huge loan.

That’s OK — they have on their hands a transformative asset, that is rising in price faster than inflation. Everybody trading this asset has agreed that it can only go higher, and will never sell at a lower price. So it seems only natural that they should spread this gospel to the world, and lift millions out of poverty!

Alex and Blair approach Cameron, their mutual friend, and fortunately, someone already rather wealthy. They persuaded Cameron to buy some Kelpies from Blair, at $1,500 each:

Total Cash (dollars)

Total Assets (units)

Asset value

Debt (dollars)

Net Worth (dollars)

Alex

$10,000

40

$60,000

$5,000

$65,000

Blair

$54,500

25

$37,500

$5,000

$87,000

Cameron

$0

35

$52,500

$0

$52,500

Price of 1 Kelpie: $1,500

Blair then takes $50,000 and buys the new car.

Total Cash (dollars)

Total Assets (units)

Asset value

Debt (dollars)

Net Worth (dollars)

Alex

$10,000

40

$60,000

$5,000

$65,000

Blair

$4,500

25

$37,500

$5,000

$37,000

Cameron

$0

35

$52,500

$0

$52,500

Price of 1 Kelpie: $1,500

Reality bites

To celebrate their new found wealth, the 3 friends decide to take a road trip in Blair’s fancy new car. Unfortunately, they got into an accident, and were all seriously injured. The medical bill came out to $12,000 for each of the friends.

No problem, they thought — all 3 friends are much richer than that, and can easily afford it.

The friends offered Kelpies to the hospital for their bills, but the hospital politely declined. As with the car dealership, the hospital simply did not have the foresight to see the transformative nature of Kelpies, and instead, demanded cash. Well, now we have a problem — our friends are asset rich, but cash poor.

Alex quickly realized that they really only need another $2,000 to cover the bills. So with deep regret, Alex offers to sell 2 of their Kelpies at the previous price of $1,500 to Blair. Alex was previously planning to sell only when Kelpies hit $3,000, so Blair is really getting a good deal here!

Blair looked at their holdings, and at the medical bill, and came up with another idea. How about, Blair sells Alex 8 of their Kelpies, at the unbelievably great deal of $1,200? This will give Blair enough cash to pay their bills, and still have $2,100 left over. And Alex got to buy Kelpies at the fantastic price of $1,200!

Cameron, too, looked at their holdings, and at the medical bill and came up with another even better idea. How about Cameron sells Alex 8 Kelpies for only $1,000 each ($200 cheaper than Blair!), and then another 4 Kelpies to Blair at the same price? That’ll give Cameron enough cash to pay the bill, and both Alex and Blair will get a GREAT DEAL!

This goes on for a while, until eventually, the friends realize, that between the 3 of them, there really is only enough cash to cover one person’s medical bills, and no amount of trading or discounting will change that fact. Also, collectively, they are now $10,000 in debt.

Stock vs flow

As alluded to in Investing vs Speculating, purely trading/speculating is a zero sum game. In our little story, the entire “market” only ever had the actual value that the friends themselves put in. Before Cameron joined the game, there was only ever $2,000 (net of debt), which was why despite their lofty “net worth”, Blair was not able to buy the car without the cash infusion from Cameron.

There never was the grandiose “value” that our friends made up in their minds, it was only ever “paper gains”, and our friends committed the sin of confusing stock with flow.

Flow – The transactions at the margin of the market

Stock – The totality of all assets in the market

Our friends thought that just because there was flow, and that the flow was consistently valuing Kelpies at a higher price, that, therefore, their stock of existing Kelpie was worth as much. This quickly breaks down, when the liquidity needs of the market participants exceeds the available flow in the market. And when that need for liquidity emerges, the phrase “prices are set at the margins” quickly became apparent.

Zero sum game?

Kelpie was just a analog for a stock, right? So, are stocks a zero sum game?

No, and no.

Kelpie is an analog for any asset that can be traded, not just stocks. This means, stocks, gold, bonds, houses, cars, bread, art, etc. Everything that can be traded. But no, that does not mean stocks (or any of the other assets listed) are zero sum games.

Remember that stocks represent fractional ownership of actual businesses. Assuming the business is performing well, it will generate profits. Even if the profits are not distributed to the shareholders, the profits exist somewhere. Unless there is fraud, that somewhere is generally “the books of the company”. This means that if Kelpie was a business, then the 3 friends could have just found another entity to buy the business from them. If the business is run well, and is profitable, it shouldn’t be hard to find some entity willing to pay for the business, although possibly at a discount — the 3 friends are desperately in need of liquidity, and thus have less leverage in making the deal with the buying entity.

In effect, a productive asset, like a stock (or bond) periodically injects the value of their production into the system, which means the entire system is a positive sum game.

For other assets, like cars and bread, which have intrinsic values (people want the car/bread, because both have attributes that are desirable), there is a natural floor to how low the prices of the assets will go. Yes, in a firesale, where the seller is desperate for liquidity, they may sell the asset for less than intrinsic value. But if the seller has enough time to shop around for buyers, they will likely be able to get fairly close to intrinsic value at least. This also means that if someone bought an asset with intrinsic value at a price higher than its intrinsic value, they stand a higher chance of losing money — unless they can find a greater fool to pay an even higher price, they will be forced to sell at intrinsic value, at a loss.

In effect, for non-productive assets, trading is basically a zero sum game — without the constant injection of value from production, the net of all trading will be $0. That said, assets with intrinsic value at least have a price floor. Assets with no intrinsic value, like our original Kelpie, will likely go to nothing eventually (technically, they revert to their intrinsic value of $0).

Productive assets at any price?

Let’s consider a stock that represents fractional ownership of a business.

At an instance in time, where the business already has some amount of assets on its books, and also has the potential to generate future profits, we are able to value the assets currently on its books, and as well as to provide an approximate value for the future profits (see the How To Value A Company series for discussions on how to value a company).

In some sense, at a specific moment in time, we can say that a business has a fixed intrinsic value, and we can treat the business as essentially non-productive, at that instance in time.

Which means that yes, like with regular non-productive assets, it is possible to overpay for a business (i.e.: stock).

The net amount of gains and losses, from all investors of [a business], across all time, based only on [the business], will be exactly equal in dollar value to the sum of all earnings of [the business].

So, you can consider trading stocks as both investing and speculating. Part of the profits from trading stocks will come from the productive part of the business (i.e.: investing), and part of the profits will come from just selling to a greater fool (i.e.: speculating).

Now, consider the P/E ratio of a company — it is the price of the company, divided by its earnings (i.e.: profits (2)). In effect, the P/E ratio is how much you pay for each dollar of profits from that company.

Remember how profits are injected into the system for productive assets, leading to positive sum games?

Let’s say we have a company with a P/E ratio of 1, i.e.: investors pay $1 for each $1 of earnings.

Every year, an equal amount of value is injected into the system as the value of the stocks. In this extreme case, the productive nature of the asset is very significant to the trading — it represents 100% of the stock value of the asset every year! In effect, if we have $1m of stock value, then every year another $1m of productive value is injected by the business, pushing our zero sum game to a sum of +100% per year.

Now, let’s consider a company with a P/E ratio of 1,000, i.e.: investors pay $1,000 for each $1 of earnings.

Every year, only 0.1% (1/1000) of stock value is injected into the system by the production of the business. In this extreme case, the productive nature of the asset is almost a rounding error — it pushes the trading from zero sum to sum of +0.1% every year.

So, the larger the P/E ratio(3), the most speculative, and more “zero sum game”y the asset.

Final words

As with our 3 friends, in the heat of the moment, when our paper net worth is rising quickly for what seems like doing nothing, it is easy to convince ourselves that we are geniuses, that we have discovered “the secret to wealth”, or that the asset(s) we are investing in has intrinsic value — who wouldn’t want to own an asset whose price is going to the moon?

But remember that unless the asset has productive value, in an emergency, when you desperately need liquidity, it may be hard to sell the asset for anything more than intrinsic value. And intrinsic value may be a lot lower than whatever price you personally paid.

It may help to think of “the asset” as “a $1 bill”. Yes, if you have a $1 bill that, for whatever reason, is desirable (maybe it was handled by some famous celebrity), you may be able to sell it to a speculator for more than $1. But the universe of people who are wiling to pay more than $1 for a $1 bill is relatively small — not everyone cares about the provenance of their cash. So the latest owner of that $1 bill, may find that in an emergency, they can really only use that $1 bill as… a $1 bill — even if they paid $100 for its provenance. In effect, that $100 “intrinsic value” applies only to a niche market, and the broader market simply does not care, and unless you can find someone else from that niche market, you are stuck with the broader market’s intrinsic value of $1.

Footnotes

For the purposes of this illustration, we are going to ignore the legality of the things discussed. Some of the things discussed here are in the legal gray area (some may be outright illegal!), so please, do not try this at home.

Earnings/profits mean something very specific in finance/accounting. Technically, the usage here is not quite correct, but it’s close enough. See How to value a company – income statement for details.

This is an oversimplified explanation. In reality, businesses grow — just because a business generates $100 in profits this year, doesn’t mean it’ll only generate $100 in profits the next year. A company with growing profits and static stock price, will naturally see a P/E ratio that shrinks with time. In effect, P/E ratio is a static, snapshot in time, valuation metric, that does not capture the dynamic nature of businesses over time.

This is a quick note, which tends to be just off the cuff thoughts/ideas that look at current market situations, and to try to encourage some discussions.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Tethered

Around the start of 2021, the “market cap” (1) of Tether (2) started increasing at a phenomenal rate. In the first month of 2021, it grew by about 25%, then 35% in February, but “only” 14% in March. April saw another 25% spurt of growth, but May and June, together, saw “only” a 22% growth, with most of the growth in May and June mostly flat, with even a slight dip in late June.

Prior to around late 2020, the crypto space was mostly the playground of more libertarian minded folks, and for the most part, ignored by most large institutional entities.

However, around late 2020, and especially in early 2021, a few large institutional players started taking note of crypto, and initiated positions in the space. The reverse is also true — the provider of Tether claims that the majority of its assets were held in more traditional financial instruments, such as commercial paper (i.e.: short term corporate debt), corporate bonds (i.e.: longer term corporate debt), funds, etc.

So — Tether is “backed” (3) by corporate debt, while some (possibly same, possibly different) corporations have crypto on their balance sheets, and finally, Tether is part of many conversion pathways between many crypto coins and fiat currencies (4).

Leverage

There is anecdotal evidence to suggest that Tether is involved in a bunch of highly leveraged (5) crypto trades, and the increased use of Tether may be a symptom of the increase in leverage in crypto in general. Note that Tether is hardly the only stablecoin — there are a ton of these currently operating, mostly tied to the US dollar, though some are tied to other fiat currencies.

Some firms issuing bonds (i.e.: debt) to buy crypto coins.

At the same time, some crypto coins (not necessarily the same coins as the ones above) are backed by corporate bonds (again, not necessarily the same as the bonds above).

Even though the coins/bonds in both those statements need not be the same coins/bonds, there will likely be some form of linkage, albeit potentially tenuous. For example, bond funds and algorithmic trading firms (i.e.: quant hedge funds) tend to lump individual corporate bonds into groups, and then trade everything in the same group as basically interchangeable.

Thirty thousand dollars under the C(oin)

Currently, Bitcoin is trading at around 31 thousand dollars, having repeatedly tested the 30-31 thousand range recently, and more broadly (since mid April) grinding downwards. Given that Bitcoin started the year just below 30 thousand dollars, almost everyone who bought bitcoin in 2021 is underwater on their 2021 purchases.

Get to the damn point

All the above is basically just a “quick” introduction to the space, and to make the following points:

Many institutions initiated crypto positions in 2021.

Bitcoin, by far the most popular crypto coin (6), is basically flat on the year. (7)

There is a lot of leverage in crypto.

There are non-trivial and often non-obvious linkages between cryptos and more traditional financial assets.

Given the above, it seems to me, that if bitcoin were to fall decisively below around the 29 thousand dollars mark (a drop of around 7%), and stay there for more than a few days, there is a decent chance that a few of the institutions may sell (or be forced to sell, due to being overly leveraged), resulting in a cascade of selling between the linked assets, as over levered players are forced to unwind.

Which is the nice way of saying “contagion”.

It probably won’t be terrible. Despite the large numbers involved in crypto, which dwarves the numbers we saw during the Great Financial Crisis of 2008, many players in the crypto space are relatively price insensitive, and many bought in before the 2020/2021 run up in crypto prices, so they may not even be underwater.

So while there may be pain (and very intense pain at that) in the linked assets during the unwinding of leverage, it probably (hopefully!) won’t result in financial armageddon like in 2008, i.e.: the pain will probably (really, really hopefully) be contained to the linked assets.

That said, it’s not clear to me that if (and that’s a very big if) such an unwind were to occur, whether the prices will quickly return to their pre-unwind values, or if they’d languish around or even go down more.

I guess we’ll just have to wait and see.

Footnotes

More accurately, the spot value of all outstanding Tether coins.

Tether is a stablecoin, a type of crypto coin whose value is supposed to be tied to fiat currencies like the US dollar.

More than a few financial analysts have questioned the Tether disclosures, since those numbers would make Tether one of the largest holders of corporate debt instruments. Yet prior to these disclosures, almost no large bank/analyst firm had Tether on their radar, which is rare. It’s possible, but unlikely.

Many crypto brokerages actually do not trade in fiat — they may not have the proper licenses with the relevant regulators. Instead, they trade only in stablecoins (i.e.: you are buying a stablecoin when you sell another crypto, and selling a stablecoin to buy another crypto). This isn’t always obvious to the end user, because these brokerages sometimes represent the trading as being against fiat currencies. One recent example is El Salvador’s law making bitcoin legal tender — users put in US dollars, which are then immediately converted into Tether, which is then used to buy the bitcoins.

I guess “highly leveraged” is a matter of perspectives. Traditional stock trading only allows 2x leverage, but crypto trading tends to allow for much more, e.g.: Kraken, Binance, etc.

Almost all institutions speculating in crypto coins are only in bitcoin, since it has the most liquidity, and is the most recognized.

In the crypto space, anything less than a 10% move over a few months is basically “flat”.

Opinions are like rear ends — everyone has one, and most of them smell funny. Analyst reports are just formal versions of opinions. Draw your own conclusions.

I want to start by noting that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, via some formal classes, but mostly self-taught.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

What report now?

The definition of an “analyst report” is a little loose — people have been talking about stocks pretty much since people have been trading stocks. Anyone who claims to be able to predict the movements of stocks will always get an audience.

To keep the discussions sane, when I say “analyst report”, I mean “analyst reports, valuation models and other stuff of this nature”. Essentially, any document (or video!) that tries to decipher the threads of Fate and give you an insight on what a stock’s price would be in the future.

Types of report

Analyst reports come in 3 main flavors – sell side reports, buy side reports and independent reports.

Sell side reports are the reports that banks, brokers, dealers, etc. generate. These are entities that generally are not investing in the stocks, but provide a service to help someone else (their clients) buy or sell stocks.

Buy side reports are the reports that hedge fund managers, private equity managers, endowment fund managers, private investors, etc. generate. These are entities that are investing in the stocks themselves, or are managing money for others who are investing.

The main difference between brokers/dealers and “money managers” in this, is that “money managers” (buy side) have “skin in the game” — if their recommendation do well, they tend to profit, and if it does not, they may lose money. Brokers/dealers (sell side), on the other hand, are generally just interested in encouraging trading activity — they collect a fee based on each trade, and have no further “skin in the game”, regardless of how the stock performs.

Independent reports are generated purely for the sake of the report. For example, independent research companies which generate reports, and then try to market and sell the reports themselves.

In terms of quality, independent reports tend to be the least biased, followed by buy side, followed by sell side.

Note: Everytime the market is moving rapidly, either up or down, there will be a rush of people trying to portray themselves as “gurus” of the stock market. Some of these people are legitimate — proper research operations with a team of researchers. Others are more fly-by-night operations with a single (or maybe husband+wife/family) operator, yet others are just thinly veiled buy side operations that are just touting their own stocks. The first may or may not produce good recommendations, but the latter two almost never so.

Why write these reports?

As hinted above, sell side reports are generally created as a means to encourage clients to trade more. For example, most brokerage firms will produce reports that provide basic information about a company, and provide historical charts of how the company’s stock price and various other metrics have performed. Some buy side reports also include projections or even recommendations on what stocks to buy and when.

The goal, ultimately, is to provide as much information as needed for the client to decide that they know enough to pull the trigger — to execute a trade. Remember, sell side earns their money from collecting fees (or spreads) when a trade happens, or by collecting fees for handling your account. If you don’t trade, and you don’t put money/assets with them, they don’t get paid.

Buy side reports, on the other hand, are generally private. They are generated as proprietary work products of large financial entities, or even your average investor! Many retail trader have some form of research report that they produce while trying to decide how to manage their money. This can be as simple as “TSLA to the moon!” scribbled on a piece of toilet paper, or as detailed as a spreadsheet with line by line breakdown of a company’s quarterly reports.

The buy side reports that generally make it to the public, usually are published with a single focus — to convince the rest of the world that they are right, and that the rest of the world should follow them in that trade.

Independent reports, finally, are usually made for sale. They tend to be more neutral in tone, and often, the goal of the report is to sell the report itself. For example, Morningstar, Motley Fool, Benzinga, Seeking Alpha all provide independently sourced reports for sale. (1)

Reading an analyst report

When you read an analyst report, you should keep in mind the main objective of the research author, as well as their competencies. As this blog clearly shows, anyone with a keyboard can put together a post. Whether that post is worth reading, is an entirely different matter!

For the most part, analyst reports are fine — they may be wrong (or right!), but they are “fine”. Which is to say — analyst reports are not always right. If you read a report in full, including all the little size 1 font wordings and maybe press the author for proper disclaimers/assumptions, you’ll quickly realize one thing:

All reports have a list of assumptions/caveats, that taken in full, will read something along the lines of, “This report is correct, assuming it is correct. It may also be wrong. Don’t sue us.”

Analyst reports are not meant to be crystal balls — they are not meant to be predictive. For the most part, they are meant to be persuasive. i.e: Given a set of assumptions, then one possibility is that “this” will happen, and you should believe me, because <reason>.

In many cases, the assumptions are simply “assuming what we saw in the past N months repeat in the next N months”. Which is “fine” — it’s a reasonable prior given no additional information, but it is not “right”, nor is it “predictive”.

When you read an analyst report, don’t just skip to the last line that says “stock X is worth $Y”. Because that line is, literally, the most useless line in the whole report.

That line bakes in the biases, prejudices and, frankly in many cases, dumb-posterior assumptions made by the author, along with whatever number/fact fudging they care to put in. Instead, read through the assumptions, and see if they make any sense. You need some amount of critical thinking, some background on the macro and micro environments, and potentially some research of your own.

Once you’re done with the assumptions, look at the model the author is building. There are many valuation models, but all of them have pros and cons. More importantly, not all models apply to all companies. For example, P/FCF is a very useful model for REITs, because of their tax structure, but P/E is completely useless (because a large part of “E” is reduced by depreciation, which isn’t a real cost for most real estate properties) (2).

Once you’ve done the above, there are a few ways to react to an analyst report:

Read more analyst reports.

Adjust their numbers that were based on wonky assumptions and/or model.

Assign a probability for each report to become true, based on what you understand about the macro/micro environment.

Then take a probability weighted average of all the adjusted results and use that result. For example, after reading 3 reports, and adjusting each for obvious errors, you get these predictions: Report 1: Stock @ $100 Report 2: Stock @ $90 Report 3: Stock @ $50 You give these reports the following probabilities of becoming true: Report 1: 50% Report 2: 40% Report 3: 10% And so, the weighted average is (100*0.5) + (90*0.4) + (50*0.1) = $91

Read more analyst reports.

Filter out those that are just plain batpoop crazy.

Of the rest, look at the inputs they use, and for each input, consider a reasonable conservative estimate across all reports (you can use the most conservative, or the 25%-tile or whatever, depending on how risk-averse you are).

Then recompute based on these numbers. For example, if you filter down to 3 reports that are reasonable, and all of these have stock price models based on some estimate of future sales and future production costs, then you can either take the median (or 25%-ile, or average, or whatever) estimate for each of future sales/costs. Plug these blended estimates into the model, and arrive at your own estimate for the stock price.

Read more analyst reports.

Use the reports to get a feel of what people “on the street” are thinking, because while a single report is probably noise, a bunch of them together may show a useful trend.

Build your own model.

Read the report as a work of fiction, just like Harry Potter. If you enjoy it, great. If not, maybe try Judy Moody instead.

Roll your eyes at yet-another-crazy-analyst-report, say something nice but vague so that whoever showed you the report, and is eagerly hopping up and down telling you about this “hot new opportunity” that is “sure to go to the moon”, will just leave you alone.

Start a thread in an obscure forum in a private company/blog, trying to explain that analyst reports are not meant to be prophetic, nor are they the threads of the Fates. And pray that enough will understand enough that they stop throwing money at terrible ideas based on even more terrible ideas.

Footnotes

This is not a recommendation nor endorsement for any of these services, or the quality of their reports. Also, note that some research branded as “independent” may have ulterior motives, such as illegal pump and dump schemes, trying to “talk the author’s book”, etc.

See the “How to value a company” series of posts for more details on valuation models:

This is a quick note, which tends to be just off the cuff thoughts/ideas that look at current market situations, and to try to encourage some discussions.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Disclaimer

My usual stance is to not write about anything that can be construed as “investment advice”, because I’m simply not qualified to provide that to anyone. This post diverges slightly from that.

In this post, I talk a little bit about my thoughts on inflation, and how I would (and currently am) hedge for inflation. This is entirely my personal belief, and what I’m doing for my own portfolio. More importantly, I may change my mind at anytime, and I may or may not write about it, and may or may not otherwise notify you when I change my mind.

Please do your own research, and consider carefully what is right for your own personal situation. What is right for me, may not be right for you.

Janet Yellin’

Janet Yellen, the previous Federal Reserve Chair and current Treasury Secretary, just had a very interesting press conference. As opposed to the Federal Reserve, which has been steadfastly saying “inflation is transitory”, Yellen gave a much more nuanced take, and suggests that higher inflation, as high as 3%, may be acceptable to the government. Given that officially reported inflation in the US is somewhere between 0 and 2% for the past decade or so, that’s pretty big news — even a 1% increase in inflation can result in significantly higher prices over long periods of time — 0% compounded for 10 years results in prices that are exactly the same, 1% compounded for 10 years leads to a ~10% increase, 2% leads to ~22% increase, and 3% leads to ~34%.

There has already been considerable consternation in the markets about higher inflation, with a scare earlier this year leading to a ~12% sell off in QQQ, and some more risky stocks dropping as much as 50-60%. So yeah, everyone’s talking aboutinflation. Yellen making it official, doesn’t seem like it’s going to help sentiments.

How high is high

Generally speaking, I think of inflation as several buckets (all numbers per annum) (1):

Note that the range for each bucket generally increases as you go down the list. This is by design — historically, inflation tends to grow exponentially (or at least, at a polynomial rate), which with some hand-waving, sort of means it’s easier to get from 6% inflation to 8% inflation (a jump of 2%) than it is to get from 1.5% to 2% inflation (a jump of 0.5%). This is also why central banks tend to, or at least, used to, be very wary of inflation — beyond medium inflation, it becomes very easy for inflation to get out of hand very quickly. When that happens it becomes really, really hard to get inflation under control.

Transitory?

The next question is, is inflation transitory? And the answer is… yes. No. Maybe?

It depends on what you mean by “inflation”. Inflation just describes a phenomenon, and therefore, technically, is always with us — even deflation is basically just negative inflation. More accurately, I think the question is, “is higher than normal inflation transitory?” And the short answer is — I don’t know.

But if I were to guess, then I think that it is unlikely that the US gets to high inflation in the near term (say, next 1-3 years). And even if it did get to high inflation, it’ll probably be transitory (say, less than 1-2 quarters).

As for medium inflation (which is still higher than the normal 1-2% we’ve been seeing), I used to think that it’ll be transitory and maybe last at most 1-2 quarters. But recent events, and Yellen’s speech, changed my mind, and I think we may see it for maybe 4-5 quarters, possibly even up to 2 years. Most of this has to do with how the economy is not really returning to normal evenly, and certain sectors are facing severe supply issues.

What I am doing

Given that I don’t think high (much less very high/hyper inflation) are in the cards, then it seems unlikely that inflation will be so high that it causes severe distress to many businesses (Some yes; Many, probably [hopefully] not).

So the core thrust of my thinking is that selective investments in productive assets (i.e.: businesses) should work. The key question is, which sectors/industries?

Bare necessities

My thinking, again, personal opinion, may be wrong, is that basic goods and services will still be in demand. So things like

Housing

Consumer staples

Healthcare

Utilities(-like)

will be in demand. And to the extent that the businesses in these industries/sectors can keep their costs under control and adjust their prices to account for inflated input costs, they should do well (3). Maybe even better than other sectors/industries. In my mind, non-“bare necessities” like consumer discretionary may suffer for 2 reasons:

Higher inflation tends to sap savings and reduce disposal income, leading to cutbacks on non-essentials.

In the past ~12 months, we’ve already seen an explosion in discretionary spending, which is likely to end once the stimulus and its effects die down; Usually, these types of pent-up spending tends to just pull forward demand, which means forward demand should be reduced — you only need so many Peloton bikes.

So, for the near term, say 1-3 years, I’m guessing the above sectors/industries will do slightly better than the others (4).

Note that for housing, I’m particularly in favor of multi-family housing, since that’s generally the most cost-effective option for the budget conscious, and for utilities(-like), I’m favoring those that are not deemed “natural monopolies” and thus heavily regulated (to the point where they cannot easily raise prices to offset increasing costs).

Can I be wrong?

You should always, always, always assume that whatever financial analysis you read has a high chance to be wrong, either intentionally (the author is malicious) or unwittingly (the author is just wrong) — nobody can see the future.

That said, here are some risks, that I can think of, to my guesses above:

Currently, various forms of fiscal stimulus are ending. If the government extends or comes up with new stimulus, then the above will likely be horribly wrong.

Currently, the Federal Reserve’s official stance is no interest rate hikes, though they are going to start talking about it. If they dramatically pull forward the timeline of hikes, or dramatically push back the timeline of hikes (I’m guessing first hike to be around 2022 – 2023), then the above may be horribly wrong.

Currently, the pandemic is ending in most developed countries, and peaking in most developing countries. To the extent that reopening proceeds at a reasonable pace (say, full reopening by end 2022 in most/all developed countries), the above is probably fine. But if not, then the above may be very wrong.

Currently, I’m not yet a complete idiot. But if I were…

Footnotes

Note that these are my personal definitions, and not firm — the boundaries of the buckets move slightly if you ask me at different times. That said, I think most economists will come to buckets that’s roughly similar. Other than the hyperinflation bucket, there are no official definitions that I know of.

This is the official definition — 50% monthly inflation, so ~12,900% a year.

It is not a coincidence that most of the sectors/industries listed are more likely to have fixed costs, but variable prices.

Note that “slightly better” is relative. It doesn’t mean these sectors/industries will go up in value — if the entire market tanks 50%, if these sectors/industries only tank 49%, they’ll still have done “slightly better”.

Everyone’s scrambling to find the next big thing, so that they can be rich. But things don’t come out of thin air, they are borne of ideas, sometimes even great ideas, and it is these ideas, coupled with a vision and hard work that resulted in the thing.

But where do ideas come from? Well, for the most part, ideas come from nothing. So really, nothing is the root of all these.

What if, we can skip all the in-between steps and just get rich off nothing? Move over Knowledge Economy, and welcome the Nothing Economy.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

So someone sold a statue. It is, at the same time, an extremely unique statue, and yet a very common one, because it looks exactly like the statue in the picture above. No, not the statue of the man, but the statue between his palm and his face — nothing. Yet, it is also unique, in that well, that nothing was presented on a pedestal, and sold for $18,000 dollars. 18,000 cold, hard, American dollars.

Nobody has ever done that before. Usually when someone wants to sell you nothing for real money, they have the decency to lie to your face like, “I’m gonna sell you this car for $18,000.” Then they take your money, make up some excuse (“I really need the bathroom, must be the oysters!”), and you just never see them again. Nothing sold. Money changed hands, somebody is happy, everybody understood what happened.

Nobody has really outright told anyone they were selling them nothing for $18,000, and then taken their money, legally and with both parties happy. It’s just not done, there are etiquettes and all that. But someone just did it, and it is unique.

Now, I don’t want to go around besmirching the good name of great inventors and all that, much less inventors of a whole new field of economics/finance, but really, I think the artist did it wrong.

Now that they’ve sold the nothing (I mean, statue), they can’t very well sell it again. It’s not theirs anymore. You simply just can’t go around selling things you’ve already sold. That’ll be fraud. And fraud is bad.

So that means all these following tips I’m gonna throw out, will be completely useless to them. They cannot act on these marvelous tips. Too bad.

Tip 1: We must go deeper

Why stop at selling the nothing itself? All the cool kids know you have to NFT it (1). An NFT is just a reference to something. In this case, nothing. That makes it even more meta. An NFT that references something is always kinda iffy, what if that something is destroyed? Or lost? Or stolen? Then that NFT seems kinda pointless, no? Wrong, even.

But if the NFT references nothing… then, it’ll.. always do the right thing? It just reference nothing no matter what. If you got burglarized, and the burglars stole nothing, you won’t call the police — what would they do? (“Sir/Mdm, they stole nothing, so we’ll do nothing, and you’ll have recovered nothing, and everybody’s happy.” ) Instead, you’ll simply shrug, and replace your nothing with nothing, and you’ll be made whole (2), and your NFT still makes sense… kinda.

Now, because the NFT is just a reference to nothing, it’s not fraud to just churn out more of it (all pointing to nothing!), and then sell them. Imagine the merchandising deals you’ll make! Disney will be green with envy.

Tip 2: … and nothing is fireproof

Why stop at selling the nothing, or the NFT of nothing? Take the next step and just burn it, make a video of you burning it, and then sell an NFT of that video. Is your head spinning yet? That’s just called art. You just need to be better at art to understand this.

Now, normally, the “burn something” NFTs are always a little bit dangerous. Sometimes it just doesn’t work out you know? Like the statue in the picture above (yes, the man this time) — it doesn’t burn very well, I’d bet. It’s all stone and clay and stuff, and those things don’t burn. Stone and clay just don’t like to cooperate like that. And other times, they burn too well. Like, burst in flames and burn down the whole building well. That’s just inconvenient. So, after you make a great big announcement about a “burn something” NFT, either it doesn’t burn (fraud!), or it burns down your house (not fraud, but potentially painful). Dangerous.

But nothing? Man, nothing burns very well all the time. Nothing burns like thermite. Yet burning nothing will never burn down your house — nothing burns until there’s nothing left, and since there’s nothing left in the first place…

And most importantly, after you’ve burnt nothing, and even if you’ve burnt everything, you’ll still have nothing more to burn!

Folks, this is a sustainable, repeatable process. And to a businessman, that’s just the sound of money. Ka-ching!

Tip 3: Franchise, franchise, franchise

Ok, I lied earlier. This tip will work for the artist. I’m human too, I make mistakes.

Now, think of all the crime’y people trying to come up with ways of laundering their illicit cash. They go through all sorts of crazy schemes to make the money seem legitimate, and in the process they lose 50-70% of the cash due to transaction costs and taxes. But really, they should have just did what the artist did.

“This cash is not illicit! I worked hard for it! I am a financial speculator by trade, and this is the profit of my trading!” I’d imagine they’d say when the police comes knocking. “What do you trade in, sir/mdm?” the police will ask, and our crime’y folks will, with a perfectly straight face, say, “nothing. I trade nothing.”

So, the tip here is just to go big! Set up a whole business built on selling nothing! Then sell licenses to operate a similar businesses under the same trade name to others — franchise the hell out of this! I can already see the mob bosses lining up to get in on a piece of this action.

What goes around…

So, we have a financial system that is entirely backed by the “full faith and credit” of various governments, i.e.: fiat money. Basically, they are backed by nothing (tangible).

The crypto fans are upset about this, and so their response is to create a better system. One based on blockchain, and math, and backed by ideas. And well, long story short, backed by nothing (tangible).

And then someone used either the first nothing, or the second nothing, to buy the third nothing. Albeit, the third nothing comes with a fancy presentation, pedestal and all that.

So I guess they got a good deal?

Footnotes

Yes, I just used NFT as a verb. I’m cool like that.

Mathematicians will tell you that not all “nothings” are the same — some nothings are better than other nothings. But that’s just mathematicians being mathematicians — they just like to get in on a good joke and make a mess of it.

This post discusses some common techniques on evaluating the fundamental value of a company by looking at its cash flow statement, for those who are investing, as defined in Investing vs Speculating.

There are, of course, other ways of evaluating the value of a company, which we will cover in other posts. Other posts in this series:

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Show me the money

If, after reading How to value a company – income statement, you come away thinking there’s way too many finance gobbledygook in there about stuff that aren’t really about cold hard cash, like depreciation, accounts payable, etc., and you’d really just want to figure out whether cash is coming in or leaving the registers. Then you may be tempted to just throw away the income statement and just scream, “Show me the money!”

And you wouldn’t be alone.

This is where the cash flow statement comes in. As the name implies, it is, literally, a statement of the cash flowing into and out of the company. Gone are the hand-wavy “assets” and “costs” like accounts receivable and depreciation. Gone are the confusing terms like “operating costs”, which for some reason, don’t include the costs of actually producing the products (what’s up with that?). Everything is broken down into 5 very simple lines, which tell you exactly how much cash is coming into (or leaving!) the company’s coffers and where they are from (or are going).

Common accounting terms

There’s really only 5 lines on the cash flow statements that are important. Yes, there are probably like 30 lines on an actual cash flow statement (we’ll get to them later), but the 5 important lines are:

Net income

This is always the first line in the cash flow statement, but always the last line in the income statement. In both cases, this is the same number, and mean the same thing.

Net income, defined in the earlier post, is the glue that joins a company’s income statement to the cash flow statement.

Total cash from operations

This is the actual amount of cash, moving into, or out of, the company, due solely to its operations.

Usually, this value is derived backwards from net income by adding back (or taking out) all those line items that aren’t strictly about cash flows due to operations.

For example, Depreciation is added back in, because it’s not an actual cash expense. Accounts payable are added back in, because we haven’t paid our suppliers yet, and the cash is still sitting on our balance! Similarly, accounts receivable is taken out, because we haven’t been paid yet.

Total cash from investing

This is the actual amount of cash, moving into, or out of, the company, due solely to investing activities. This includes things like buying new factories, new equipment, buying another company, etc.

For example, If our company buys a new factory for $100,000, then this value is reduced by $100,000. If our company sold a previously bought factory for $120,000, then that is reflected as an increase of $120,000 in this value. If our company did both, and had no other investing activities, then the total cash from investing = -$100,000 + $120,000 = $20,000.

Total cash from financing

This is the actual amount of cash, moving into, or out of, the company, due solely to financing activities. This includes things like taking out a new loan from a bank, paying off an old loan, paying a dividend to shareholders, etc.

For example, If our company took out a new loan of $10,000, and paid off an old loan of $9,000, then the total cash from financing = $10,000 – $9,000 = $1,000.

Net change in cash

This is the actual change in the cash balance of the company.

This is simply “cash balance before this period” + “total cash from operations” + “total cash from investing” + “total cash from financing”.

Sometimes, there’s a little line entry that adds or removes a little bit additional due to things like foreign exchange fluctuations. Just to spice things up a little bit.

Showing your work

Yes, there’s really only 5 lines that matter. But you know how things are. We can’t make life too simple — where’s the fun in that? In general, a cash flow statement will contain, oh, about 30-50 lines. The lines other than the 5 lines mentioned above, are basically just the accountants showing their work.

Like in elementary school math, where you can’t just write “5”, or even “The answer is 5”. No, you have to write: Sally has 2 marbles. Peter has 3 marbles. Total marbles = 2 + 3 = 5.

The result is the same. But the teachers prefer the latter. It makes them feel happier. Or something.

This is good for us! Sometimes the accountants (or the company itself) get things wrong. So they show their work on the cash flow statement. And we get to decide if they know how to do basic arithmetic. (1)

One thing to note: numbers in parentheses are negative numbers — cash flowing out of our company. For example, in the “cash from financing activities” section, “(5,000)” generally means we paid off $5,000 in debt. The parentheses means cash flowing out, and numbers without parentheses mean cash coming in.

And now what?

From the cash flow statement, we can discern a few very important tidbits: Is most of the cash coming into the company via actual operations? Or is the company being propped up by more and increasing debt? Or by selling off assets?

Ideally, we want “total cash from operations” to be a positive number, and much larger than “total cash from investing” and “total cash from financing”.

Even better if “total cash from financing” is a negative number (we are doing so well, we can pay down debt!). Note that a positive “total cash from financing” number isn’t necessarily a bad thing. Maybe the company is raising debt to buy out a competitor and thus expanding its businesses. Or maybe the company is developing a new product line, etc. One off debt issuance to invest into the business is usually a good thing! The red flag is when “total cash from financing” is always positive (i.e: the company is always issuing debt), and always a substantial amount compared to “total cash from operations”.

“Total cash from investing” should hopefully also be a negative number, indicating the business is likely profitable and the company is investing more money into it. However, this is more nuanced.

If “total cash from investing” is always negative, and always a large absolute number, that may indicate a business that is heavily dependent on new injections of capital. For example, if a company has $1,000,000 of “total cash from operations” every quarter, but also $(900,000) of “total cash from investing” every quarter, that suggests that perhaps the company is heavily dependent on rolling over its investments every period to generate the profits for the next period.

Companies like this are sometimes at the mercy of their customers — if they also have a large accounts receivable, if their customers fail to pay up on time, these companies may get into temporary liquidity distress.

Even without being at the mercy of their customers, these companies generally don’t tend to perform as well — the need for heavy capital reinvestment makes it hard to scale the business, because it is not always possible to find enough capital to deploy; At the same time, the need for heavy capital investment (as a ratio of operating profits) suggests lower profitability, which deters investors.

Free cash flow

Free cash flow tells us the core efficiency of a company’s businesses — It is simply the cash the operations of a company generate, without consideration for reinvestments (i.e.: capital expenditure).

Recall that “total cash from operations” is the cash a company generates ignoring depreciation and amortization (amongst other things). So, by starting with “total cash from operations”, we just need to take out “capital expenditure” to get free cash flow:

“Capital expenditure” is the amount of cash a company reinvests in its businesses. For example, to replace capital assets that were consumed as part of operations, or to scale the business. This is sometimes called out in the cash flow statement or income statement, but usually needs to be estimated or calculated — by looking at the income statement and deducing which line items are related to capital expenditure.

Free cash flow = total cash from operations - capital expenditure

Another form of free cash flow, unlevered free cash flow, is simply free cash flow assuming the company has no debt. In this case, interest expenses are added back to the value of “free cash flow”, while tax breaks for interest expenses are taken out:

Unlevered free cash flow = free cash flow + interest expenses - tax deductions due to interest expenses

Note that tax deductions due to interest expenses may not appear in the cash flow statement nor the income statement, and may have to be estimated.

Free cash flow essentially tells us “how much this company can return if we just run it ‘into the ground'”, i.e.: without replacing consumed capital assets. It is a base case of what profits the company is capable of extracting from its businesses.

Unlevered free cash flow is similar, and gives us an idea of what free cash flow would look like, if an acquirer buys out the company and pays off all its debts.

There are other variants of free cash flow that are sector specific. The most widely used is “funds from operations”, which is used commonly in real estate heavy companies (such as REITs). “Funds from operations” is just unlevered free cash flow with losses and gains from sale of properties removed, i.e.: gains are taken out, losses are added back in. The idea is similar — to try and get a number that gives us an idea how profitable this company can be, purely from its core operations.

Once we have determined the variant of free cash flow we are using, and have computed its value, the next question is, what do we do with this number?

Recall that free cash flow gives us an idea of the core efficiency of a company at its businesses. So the most common thing, is to look at free cash flow over time. Is it consistently going up? Is it growing at a suitable rate based on investments into the businesses? How much is the shareholder paying for each dollar of free cash flow?

Ideally, we want free cash flow to be increasing over time, and at a pace equal or faster than reinvestment rate — if the company is reinvesting profits equal to 20% of capital assets, then free cash flow should increase by 20% or more in subsequent periods (2). Otherwise, the company would probably be better off investing that money in other pursuits, or returning the cash to investors.

Sometimes, an unprofitable company may be a good investment, even if free cash flow is currently negative! A company that is heavily investing in its businesses may sometimes have negative free cash flow — recall that free cash flow is operating cash flow – capital expenditure. Assuming the capital expenditure is a temporary event (3), when the need to invest in scaling the business stops, free cash flow will likely quickly jump to positive. Note that such businesses are not without their risks! There is a chance that the capital expenditure does not result in future profits, for example, if the research failed to find anything useful, etc.

Finally, the price / free cash flow (P/FCF) ratio is a useful indicator of how much the investor is paying for dollar of free cash flow from the company. As with the other price ratios (P/E, P/S, etc.), the numerator is usually the market capitalization (price per share can also be used if free cash flow is also normalized to free cash flow per share).

Like the P/S ratio, the P/FCF ratio may be useful for informing whether a company is a good investment at a certain price, even if the company is currently unprofitable. Furthermore, the P/FCF ratio is also useful for companies that have strong and stable cash flows (such as some real estate related businesses) — unlike the P/E ratio, the P/FCF (or P/FFO — price per funds from operations) tends to provide a more stable value less affected by one time events that are not related to the core operations.

A company with a good P/FCF ratio, but a terrible P/E ratio may simply be affected by accounting quirks like depreciation and amortization rules, which are not strictly part of the core operations.

Footnotes

I kid! Nowadays, every financial statement pushed out by a public company, especially a large, public company, is scrutinized by an army of analysts whose jobs are, in part, to make sure silly arithmetic mistakes are rooted out. The additional lines are still useful for those who are curious, and want to know the breakdown even more, though.

Note that in some industries, there is a significant lag time between when investments are made, to when profits from those investments can be extracted. This should be taken into account when judging if free cash flow is growing at a rate commensurate with the investment rate.

Many types of businesses are characterized by heavy capital expenditure in a few years, followed by many years of extracting profits from those capital expenditures. For example, research and development heavy industries (pharmaceuticals, some technology firms, etc.), manufacturing industries (building factories, etc.). Once the capital expenditure is done, the company may be able to enjoy many years of profits without having to do more capital expenditure.

This is a quick note, which tends to be just off the cuff thoughts/ideas that look at current market situations, and to try to encourage some discussions.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Tell me what you see…

Here is a picture of the (futures) markets as of this writing:

I took a look, and the first word that comes to mind was “angry”. Angry. The futures markets look angry.

Crypto

Unless you’ve been hiding under a rock (and maybe even if you have), you’ll know that cryptocurrencies and the US stock markets have been on fire. Cryptocurrencies gained around 3x (as measured by Bitcoin) from the start of 2021 to around mid April. Then, a series of unfortunate events (which mainly rhymes with Melon Tusk) occurred and everything started going down in fits and starts.

Today, or rather the past 24 hours, Bitcoin went down roughly 18% (as of this writing), though at the peak it was closer to a 30% drop. While Bitcoin has recovered from the lows, the current price action seems to suggest more downside in the near future.

Will it go down more? Or will it rebound? Who knows? A 30% drop in Bitcoin is basically par for the course. It’s something that happens so frequently that you can probably set your clocks to it. And at least all the previous drops have seen Bitcoin recover, and then some. Though in some cases, it took years before it eclipsed the prior highs.

Stocks, again

To round back on the main topic of the day. I had a not so immodest thought, that maybe the speculative fervor in stocks and crypto are linked. Maybe, it’s just an expression of excessive money sloshing around the system, and mostly in the hands of people who are ill-prepared to deploy them wisely, leading to excessive speculation and, in many cases, outright gambling.

So, if the underlying causes are the same, and the folks frolicking in these playgrounds are the same, then maybe, just maybe, when one goes down, the other goes down with it?

In some sense, this is an extension of what I’ve wrote before (see quick note on April 20) — those things which were going up a lot, seems to be hit the hardest, and crypto, with its absolutely mind-blowing out-performance year to date, seems to be first in line to take it on the chin.

To be fair, almost everything is going down today. So it could also just be a garden variety “batten down the hatches and sell everything” panic.

Or it could all recover tomorrow, as if nothing had happened. Yes, I’ve had a lot of practice saying a lot of words, and yet saying nothing.

This is a quick note, which tends to be just off the cuff thoughts/ideas that look at current market situations, and to try to encourage some discussions.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Usually, when a company goes public, it is so that they can sell shares to the public and raise money. In that moment (traditionally an IPO, but Coinbase used a “DPO”, direct public offering, where it sells directly in the market instead of to market makers), the startup-soon-to-be-public-company is supposed to sell as many shares as it needs, so that it can fund itself until it becomes profitable, after which, it can fund itself perpetually.

Usually, a company does not need to raise debt, nor sell more shares for a while after it goes public, because, well, they generally have a good idea of how much cash they need, and with a marvelous invention called a calculator, they can generally figure out how much shares they need to sell in the IPO pretty accurately. To have to sell bonds so soon (Coinbase went public only about 1 month ago) is highly unusual.

Even more surprising, Coinbase’s DPO sold pretty well! Coinbase had expected to sell shares at around $250 a piece, but instead, it sold them at a high of $400 a piece (2). That’s a 60% upside! And since it’s a DPO instead of an IPO, Coinbase should have been able to keep that additional upside.

Even more even more surprisingly, the convertible bonds are being sold with basically no coupon — 0% – 0.5%. While the market will likely price it at some yield (by paying less than par for the bonds), generally the coupon is in the ballpark of the initial yield the issuer expects the bonds to sell at. Now, what are convertible bonds with basically no yield? Aren’t those just… options (1)?

So, again, why is a company, barely 1 month old in the public markets, selling options to the public?

Footnotes

Technically, warrants.

I found out after this post went out that Coinbase didn’t sell any shares in the DPO, only the insiders did. This is even more bizarre. A company of Coinbase’s size and operations, should be able to predict cash needs at least 2-6months in advance. So if they are raising cash because of a liquidity issue, then they should have known this months before the DPO. Why not just sell some shares in the DPO alongside the insiders? Or do the bond offering before the DPO (or bring on additional investors while it was still private)?

It’s not a good look when insiders get to sell to the public at ~$400 a share, and then the public gets diluted almost immediately by the bond/option offering… after the stock already fell 30+% to ~$250.

I recently chanced upon some benchmark numbers of the new(ish) Apple M1 chip, and the results were rather surprising. Like all good little engineers, I started digging deeper, and frankly, what I found WILL BLOW YOUR MIND! (1)

Note that this post is mostly a nerd-out. But there is a finance bit to it. If you are only interested in the finance bit, skip to the Wild guess section below.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Disclaimer

Before we begin, I want to note that I am not an Apple fan. At least, not a traditional one. I do have iPads (multiple over the years), iPods (multiple over the years, and technically, my wife’s), and various other Apple services/products.

But for computers, I’ve always been a DOS/Windows/Linux kind of guy. I’ve never owned a Mac of any form (except assigned by work), and I’ve never owned an iPhone.

An impressive little package

I stumbled across a bunch of blog posts and videos and whatnot’s, and it’s probably not very useful to link all of them here. So I’ll just link this one video (2), start at the linked timestamp (around 8m30s). There are a lot of issues with the methodology (3), but it presents a fairly accurate picture based on my understanding of the other blog posts/videos.

In short — the new M1 chip from Apple seems to be outperforming both Intel and AMD chips by a fairly large margin. This particular video is against mobile chips from Intel and AMD, though other sources suggest that general trend carries across to desktop chips. This out performance is also generally true for both CPU and GPU intensive benchmarks. Most importantly, the Intel and AMD chips, are sometimes packaged in machines multiple times more expensive.

The only times the M1 has conclusively lost are generally in one of these categories:

Benchmarks where more than 4 CPU cores are involved — the M1 only has 4 “performance” cores, so loses out in these benchmarks.

Benchmarks where an external GPU is used — M1 machines don’t seem to work with eGPUs (at least, none of the comparisons I’ve seen included M1 machine+eGPU).

In GPU-intensive benchmarks, and depending on the eGPU, the M1 generally loses by a fair margin.

You do not make potato chips with apples

Apple is not a traditional manufacturer of chips. Yes, they’ve dabbled more and more in recent years, mostly for their iPhones/iPads, but most people think of Apple as more of a purveyor of “final packaged products”, instead of a player in the chips space, like Intel or AMD, both of whom have decades more experience.

There have been many, many other players who have tried to take on the chips space. For the most part, they are either gone or have gone niche — Intel, AMD, nVidia (for GPUs) remain the undisputed heavyweights in this space.

So what is Apple doing, challenging the champions… and seemingly winning?

Golden Apple

On a different note, Apple has also been, traditionally, a manufacturer of higher end products (“lifestyle” products), and the prices they charge tend to reflect that. While they have made forays into the lower end of the consumer market in recent years, people still generally associate Apple with “expensive but good”.

And then the M1 comes along, plonked into relatively affordable machines like the Mac mini, new iPads, MacBook Air, etc., many of which start below the psychological $1,000 barrier. For reference, my first ever computer (in the 80’s) was a $2,000 beast (in size) that probably has less firepower than the modern day handheld calculator.

So it is doubly confounding, that these relatively cheap Apple machines are beating the traditional champions housed in machines that are much more expensive.

Wild guess

A long time ago, chip manufacturing was tightly coupled with chip design — Intel (or AMD, etc.) designs a new chip, and then manufactures that chip in their own foundries. So a large part of a chip manufacturer’s ability to deliver superior products, was based on their ability to research and come up with better chip manufacturing (as opposed to design) techniques (4).