Foreword

For most people, retirement/financial planning (1) is often thought of as simply how you deal with excess money (disposable income) after paying for living expenses, taxes, etc.

In my opinion, that is a very limited and limiting way of thinking about some of the most consequential decisions you would have to make in your lifetime.

As usual, a reminder that I am not a financial professional by training — I am a software engineer by training, and by trade. The following is based on my personal understanding, which is gained through self-study and working in finance for a few years.

If you find anything that you feel is incorrect, please feel free to leave a comment, and discuss your thoughts.

Human net worth

As I’ve discussed in “Net Worth“, net worth and cash flow are related topics, and in general, outside of less common cases like illiquid non-cash flowing assets, they can be thought of as the same thing.

Now, if you subscribe to that view, then it may seem odd that when people talk about net worth, they very rarely talk about their incomes from their jobs. In a hand-wavy, abstract sense, you can think of your knowledge, health and age as assets, and your knowledge + health + age enable you to generate cash flow via using your labor to create value for others, i.e. performing a job and getting paid for it.

So, in that sense, your knowledge + health + age should have some implied “worth”. In a more crude sense, you can imagine (a) someone who’s 26, but terminally ill and bed-bound, (b) someone who’s 80 but healthy for their age and (c) someone who’s 26 and healthy for their age. Clearly, in most cases, (c) will be able to generate much more income from their labor than (a) or (b).

Now, and again, being crude, if we were to put a number on it, how much would we value our knowledge + health + age?

Job incomes tend to be fairly stable and dependable in the short/medium terms(2), but health and age deteriorates with time, while knowledge improves with time, though deteriorate beyond some point due to old age. Unlike most financial assets like bonds, stocks, etc., the value of knowledge + health + age is extremely hard to compute, as there are other factors that muck things up — e.g. you may be a natural genius in the medical field, but were never afforded the chance to attend medical school and thus your genius is entirely trapped as “potential”.

Without going too much into theoretical modeling, I’m just going to use something simple — take your expected retirement age, subtract your current age. This is your number of working years left. Multiple that number by your current pretax salary, and we’ll call it your “human net worth”. This simplistic model assumes your salary increases at the rate of inflation, and doesn’t change other than that. It also assumes that the rate of discount is just the rate of inflation, so we can use current nominal values in place of imputed future discounted values. Feel free to nerd out and use more complex models.

If you’ve done the exercise above, you’ll quickly notice that your “human net worth” is probably pretty significant. If you are below the age of 35, I’m guessing your “human net worth” is probably quite a bit higher than your “financial net worth” (3).

Think like a business person

The one thing that most successful business people know, is how to maximize the value of their assets by focusing on what’s important. For example, it simply doesn’t make sense spending a lot of time trying to save a few thousand dollars by being draconian on office supplies if you are a multi-billion (or even trillion!) dollar software company. The same amount of effort, if directed towards more productive endeavors like improving employee productivity, would yield far greater results.

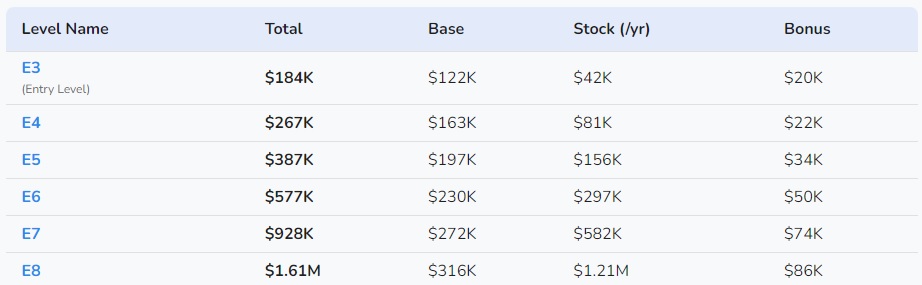

In a similar vein, if you are a software engineer with a portfolio of, say, $300k, and an annual salary of $184k, it simply doesn’t make sense spending a lot of time trying to optimize your portfolio. Even if you manage to outperform the market by 10% (assuming market returns is 10%, this would be a 20% return) (4), you will only make about $30k more. If you spend your effort concentrating on your career, getting promoted just once can easily yield more than double the benefits:

Clearly, the exact numbers depend a lot on your personal situation, but the point is that in many cases, especially for those who are below the age of ~40, where you simply haven’t had enough time to accumulate a significant portfolio, your best financial/retirement planning move is very likely to just be throw your money into something simple to manage and not too risky, and then concentrate your efforts on developing your career.

Always do the math

Many people dive headlong into finance and investing, others take up side hustles, thinking that they can supplement their main sources of incomes. In many cases, they completely ignore the one thing that is most likely to benefit their financial situations the most profoundly — simply doing better at their day job (and getting recognized for it via higher commissions or promotions), or finding another line of work with more advancement opportunities.

Before diving headlong into any new endeavor, it probably makes sense to just spend a week or two figuring out if the effort is even worth it, or if you could get more out of your efforts if you just redirect your focus elsewhere.

Personal experience

Some random notes based on personal experience and talking to people:

- Many people think real estate investments are passive (6). They are not.

- If you are owning the property outright, then you have to deal with managing the property (or paying someone to manage it, and then managing the property manager). If you only have 1 or 2 properties, this is probably not a big deal, but does take quite a bit of time. If you have more than 5 or 6 properties, this easily becomes a full time job.

- If you are investing via a fund or syndication, then you’ll have to spend a lot of time sourcing deals and vetting sponsors, reading their periodic reports to make sure everything is on track and deciding how to deploy your future dollars. In some ways, this is very similar to the pros/cons of investing in stocks.

- In both cases, you’ll have to understand the economics/finance of real estate investing, and how macroeconomics affect it and thus you. Keeping up with these generally involve a lot of reading, attending conferences/webinars/seminars, etc., which again take up a lot of time.

- Many people think trading stocks can be passive — once you’ve figured out a winning strategy, just make a bot and watch the money roll in. It doesn’t work this way.

- As someone who has written and ran multiple trading bots before for personal trading, and who has worked in a quant hedge fund, I can assure you that it is not so simple.

- All strategies eventually lose their edge. It may be 1 week after you find the strategy, or it may be 1 year. But it eventually happens. And the tricky part is trying to figure out if your current losses are due to a change in the regime (i.e. your strategy losing its edge) or just an expected drawdown. Deciding wrongly will be punishingly expensive.

- The trading space is unbelievably crowded. Outside of large funds, millions of personal traders trade either as a full time job or with bots. Thus, you’ll need to be nimble, and be able to change and adapt depending on financial/economic forces, so that you can stay one step ahead of the competition.

- Again, all the above means that a long term successful trading operation is almost always a full time job.

- If you are a software engineer (7), then unless you have $10m+ in your portfolio, your best path to financial security is almost definitely to improve yourself so that you can perform your day job better, and get to your “terminal level” (8) as quickly as possible. As shown by surveyed salaries of Facebook software engineers (5), each promotion comes with a pretty hefty and permanent (9) salary increase, each of which would easily equal a double digits return on most common portfolio sizes for people of those income levels.

- Of course, if you are personally interested in finance, and are doing it as a hobby, then by all means go ahead. All work and no play makes Jordan a dull kid. But be sure to understand the limitations of this, and do not fool yourself into thinking it is something beyond what it really is.

Footnotes

- Many people treat retirement planning and financial planning as different things. They aren’t really — it’s probably more accurate to think of retirement planning as a facet of financial planning, the goal of which is to, naturally, retire by some age.

- This isn’t true for everyone, but generally true for most people under most economic circumstances.

- “Financial net worth” is a made up term, here meaning the traditional “net worth” definition — the net value of your assets.

- It’s pretty damn hard to consistently beat the market by 10%. Many hedge funds get paid millions/billions of dollars just to beat the market by 2-3% every now and then.

- I am not endorsing the numbers on levels.fyi for Facebook. I do not know if these numbers are accurate at all, though I assume they are close enough to be a reasonable comparison in this case.

- Here, “real estate investments” mean private real estate investments, not buying publicly traded REITs, etc. Buying publicly traded REITs have all the usual pros and cons of trading stocks, which are touched on later.

- I’m specifically calling out software engineers here, because I am one, and understand the economics here better. Other professionals may have similar dynamics, I simply do not know.

- Due to luck, experience, knowledge, life commitments and other factors, most people have a “terminal level” beyond which they find it hard to impossible to get promoted beyond. At Facebook/Google/Uber and most tech companies with a similar level structure, this is generally around levels 5 – 7.

- OK, fine, it’s technically not permanent. But it’s pretty rare (outside of sign on bonuses and dramatic market events) to see annual total compensation drop at one of the big tech companies.